Determining the dollar value of your unsold merchandise—your ending inventory—is crucial for any retail business. You need this number to calculate profit, manage taxes, and make smart buying decisions. But physically counting every item can be overwhelming, especially for stores with thousands of products (like grocers or apparel chains).

That’s where the Retail Inventory Method (RIM) comes in. It’s an accounting shortcut that lets you estimate the value of your inventory at the end of a reporting period using retail prices, making your life much easier.

What is the Retail Inventory Method?

The Retail Inventory Method is a technique used to estimate the cost of your inventory by working backward from your retail (selling) prices. It’s ideal for businesses that deal with a large volume of similar, low-cost items, where the margin (or markup) is relatively consistent.

The core assumption is simple: If you know the average relationship between what you pay for merchandise (cost) and what you sell it for (retail price), you can apply that same relationship to the merchandise you have left over.

This method requires you to track four main values over a period (such as a month or quarter):

- Cost of Beginning Inventory: What you paid for the items you had in stock when the period started.

- Cost of Purchases: What you paid for all the new items bought during the period.

- Retail Value of Beginning Inventory & Purchases: What you expect to sell all those items for.

- Sales Revenue: The total sales you made during the period.

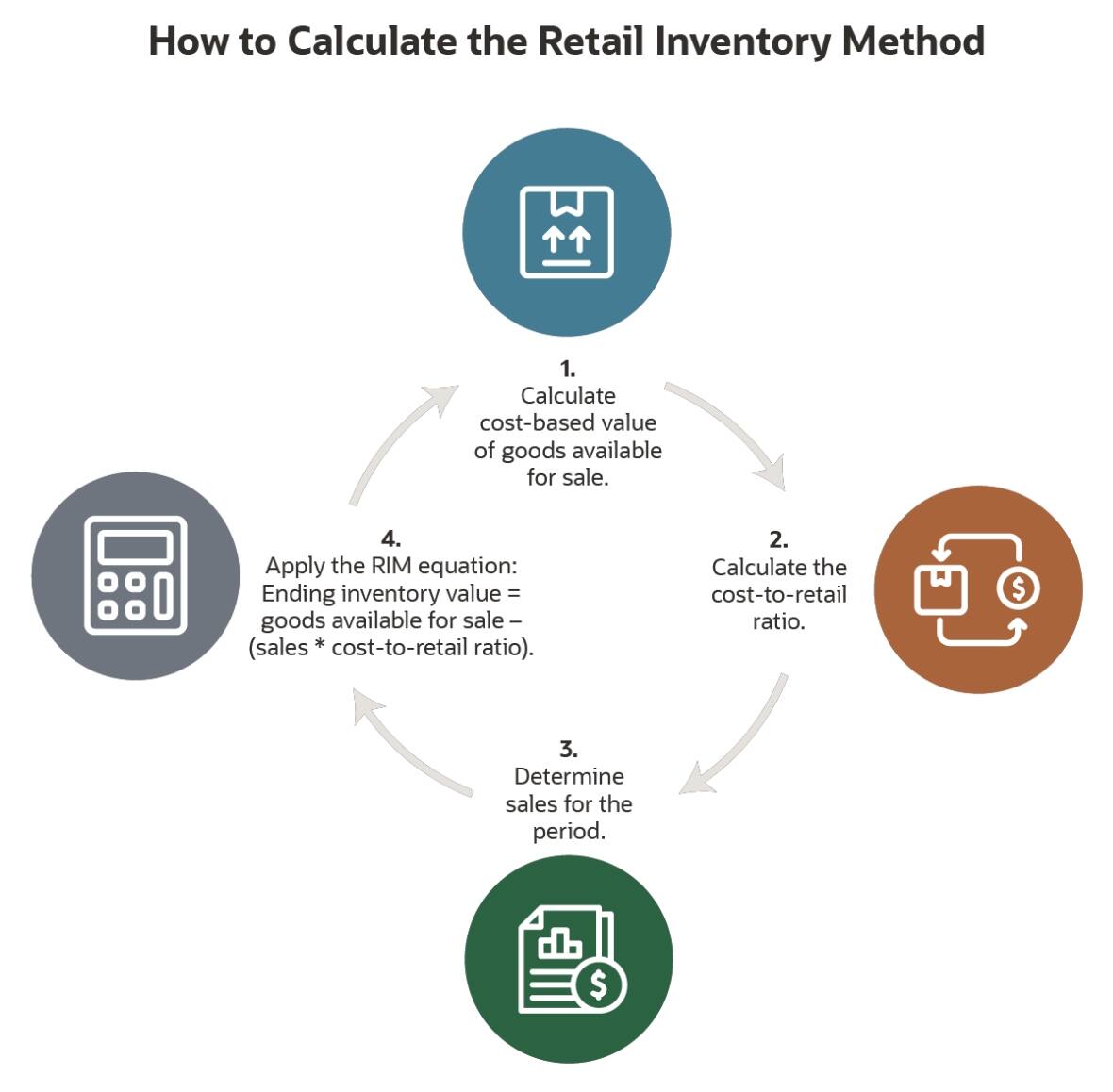

How to Calculate Your Ending Inventory Value

Using the Retail Inventory Method involves four straightforward steps to arrive at the estimated cost of your ending inventory.

Step 1: Find the Cost-to-Retail Ratio

This ratio is the bedrock of the entire method. It tells you the average relationship between your wholesale cost and your retail selling price, expressed as a percentage.

$$\text{Cost-to-Retail Ratio} = \frac{\text{Cost of Beginning Inventory} + \text{Cost of Purchases}}{\text{Retail Value of Beginning Inventory} + \text{Retail Value of Purchases}}$$

Example:

- You had $10,000 worth of goods (at cost) at the start, and bought $40,000 more (at cost). Total Cost = $50,000.

- The retail price for that same total merchandise is $100,000.

- Ratio: ($50,000 / $100,000) = 0.50 or 50%.

Interpretation: On average, every dollar in sales includes 50 cents of original merchandise cost.

Step 2: Calculate Goods Available for Sale (at Retail Price)

Determine the total maximum possible sales you could have generated from the inventory you had on hand during the period.

$$\text{Retail Value of Goods Available for Sale} = \text{Retail Value of Beginning Inventory} + \text{Retail Value of Purchases}$$

Example: $20,000 (Beginning Retail) + $80,000 (Purchase Retail) = $100,000 (Total Potential Sales)

Step 3: Calculate Ending Inventory (at Retail Price)

Now, we figure out the retail value of the items that didn’t sell. We simply take the total potential sales (Step 2) and subtract your actual sales revenue for the period.

$$\text{Ending Inventory at Retail} = \text{Retail Value of Goods Available for Sale} – \text{Total Sales Revenue}$$

Example: $100,000 (Goods Available) – $70,000 (Actual Sales) = $30,000 (Retail Value of Remaining Stock)

Step 4: Convert Ending Inventory to Cost

This is the final step. We take the retail value of the remaining inventory (Step 3) and multiply it by the ratio we calculated in Step 1. This converts the retail price back to the estimated original cost.

$$\text{Ending Inventory at Cost} = \text{Ending Inventory at Retail} \times \text{Cost-to-Retail Ratio}$$

Example: $30,000 (Retail Value Remaining) $\times$ 50% (Ratio) = $15,000

Conclusion: Your estimated value of unsold inventory (your Ending Inventory at Cost) is $15,000.

Why Should You Use This Method?

The Retail Inventory Method offers fantastic benefits, especially for managing large volumes of merchandise:

- It Saves Time: You don’t have to track the specific cost of every individual item sold. Once you have your ratio, you can quickly estimate inventory costs for any reporting period without a full physical count.

- It Improves Forecasting: Because this method uses a broad average of your costs and sales, it gives you a clear, smoothed-out view of your overall profit margin. This data is excellent for making better decisions about how much to reorder and how to price your items in the future.

- It’s Easy to Understand: The formula is straightforward. Anyone can quickly see the relationship between sales, costs, and remaining value, making it simpler for management and accounting teams to make quick decisions.